How Warren Buffett Invests in Stocks - Investment Criteria for Success

Willem

How Warren Buffett Invests in Stocks

By Willem / Originally published: 13 October 2019 / How to Invest

Table of Contents

- 1. The Four Investing Criteria of Warren Buffett

- 2. Businesses We Understand – Circle of Competence

- 3. Favorable Long-Term Prospects

- 4. Management – "Operated by Honest and Competent People"

- 5. A Very Attractive Price - Margin of Safety

- 6. Concentrated Investing – Why Warren Buffett Does Not Overdiversify

- 7. Warren Buffett's Simple Investment Advice

- 8. Summary

Warren Buffett gave many insights about how he invests in stocks over the years. In the previous article we discussed the investing philosophy and investing principles of Warren Buffett. This article looks at how Warren Buffett invests in stocks by explaining his investment criteria for good businesses. Warren Buffett uses four criteria to determine if a stock would be a good buy. In addition to the four criteria, we will discuss his investing advice that is suitable for most investors.

The Four Investing Criteria of Warren Buffett

In his Letters to Shareholders (e.g. the one of 1992), Warren Buffett explains that he and his partner Charlie Munger look at four criteria when they invest in stocks:

"We want the business to be one (a) that we can understand; (b) with favorable long-term prospects (economics); (c) operated by honest and competent people; and (d) available at a very attractive price."

These investing criteria still apply, although the last one changed from a "very attractive price" to a "sensible price". This reflects the importance that is placed on buying a very good business to a fair price. This is far better than buying a mediocre business for a good price according to Warren Buffett.

Businesses We Understand – Circle of Competence

Before Warren Buffets invests, he first asks himself the question if he understands the company. If not, he will simply move on to another company.

"If a business is complex or subject to constant change, we're not smart enough to predict future cash flows"

Sticking to sectors and companies you can understand is also known as staying within your "circle of competence".

Circle of Competence

Warren Buffett focuses on businesses that he understands (the circle of competence). No one can understand all the sectors and companies. So, it's better to focus on what you know. This leads to higher confidence in your predictions of a company's future cash flows.

A good example of a stable business is Coca Cola, a consumer goods company. The taste preferences of consumers for Coca Cola is rather stable over the years. People will still drink Coca Cola in 10, 20 years and beyond. Actually, Coca Cola was invented in 1886 and is still popular today. This means that Coca Cola can ask a couple of cents more each year for its Cola. Coca Cola is such a strong brand, that it has pricing power. Consumers are willing to pay more for Coca Cola brand than for an unknown brand. This is an example of what Warren Buffett calls a "moat". That means that the business has an advantage that is hard to capture by another company. Simply put, investing in such a company means higher chances for sustainable profits over the years.

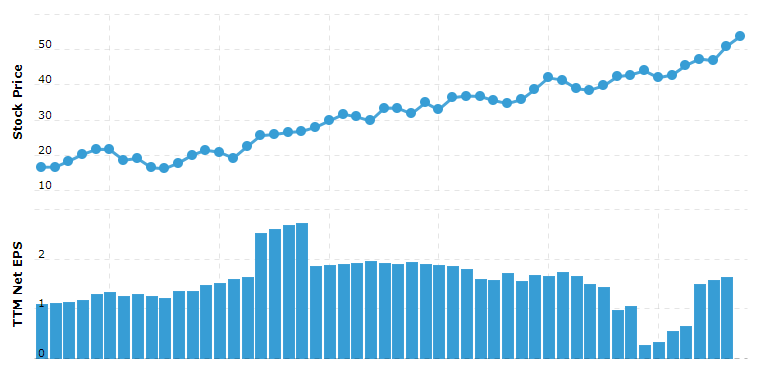

The graph of the earnings of Coca Cola shows that there was a steep decline in 2017. This was due to a one-time tax charge. However, the share price of Coca Cola has steadily advanced over the years. As did the dividends, which is raised each year for the last 50 years.

Figure: earnings of Coca Cola 2006-2019 Source: macrotrends.net

Furthermore, you need to understand the sector the company is operating in. What makes the company better than others in the sector? Be honest to yourself. For most of us, a biotech company can be very hard to understand. Buying such a company is just speculating instead of investing if you don't know what you're doing.

Favorable Long-Term Prospects

The next question to answer is if the business has favorable long-term prospects. Does the business still exist in 10 years and can it still produce a healthy cash flow? This is much easier to predict for a business that is stable and understandable. We can be quite certain that Coca Cola is still around in 10 years due to its moat. The moat is essential for long-term success of a business. Will the competitive advantage last? How hard or easy is it to create a second Coca Cola or Apple for instance?

You can imagine a good business as a castle with a big moat around it and an honest king who is guarding and protecting it. So, this means having for example a cost advantage (like Costco or Walmart) that is very hard to successfully attack by the competition. Competitors would probably lose too much money before they can successfully conquer the castle of Costco (Costco operates membership warehouses in the customer staples sector).

Important Financials of Warren Buffett

Let's cover some financial metrics before we look at the next investing criterium. Businesses with a durable moat often have superior financial metrics over sustained periods of time. Warren Buffett is especially keen on:

1. Free cash flow (owners' earnings)

2. Return on Equity (return on net tangible assets)

3. Margins

4. 1 dollar retained must create 1 dollar of value

Cash Flow Example and Return on Equity

The table below shows that Coca Cola was able to generate positive free cash flows during the last 10 years. Warren Buffett likes to see that the company has a proven moat which shows up in the financials. He does not like buying companies without a good financial track record. The focus is on consistent companies that produce healthy cash flows. This limits the chance of losing money by buying a company that has not yet proven itself. The free cash flow tells you how much cash is available to, for example, pay-off debt and to pay dividends.

The free cash flow is deemed superior to net income as it is less sensitive to accounting tricks and tells how much cash the business generates after capital expenditures. Capital expenditures (capex) are not only needed for growth, but also for maintenance of buildings and machines. Additionally, capex is needed to keep an edge over the competition. That's why Warren Buffett always takes into consideration the capex and does not look at EBITDA (earnings before interest tax depreciation and amortization).

Coca Cola's cash flow 2009-2018 Source: Morningstar.com

Warren Buffett actually looks at "owners' earnings" which is similar to free cash flow but separates the capex in maintenance and growth capex. Often this is hard to find in the annual report. Looking at the free cash flow is more conservative is such a case.

The next one is return on equity (ROE) and return on invested capital.

ROE = (net income / equity)

ROIC = (operational earnings (also known as EBIT) / debt + equity).

Note that ROIC includes both debt and equity, so operational earnings (or EBIT) is used as interest must be paid to the providers of debt. So, you need to include interest in the numerator for the ROIC calculation.

Warren Buffett looks at return on net tangible assets (this will be explained in a later article). For now, we focus on return on equity to keep things simple. ROE is the return shareholders get on their investment. A high ROE reflects great business economics and shows that investments of a business generate money for shareholders. Coca Cola is able to generate very healthy returns on their investments. A good ROE depends on the sector, but generally a ROE of more than 15% is very good (learn more about ROE here).

Coca Cola 2009-2018 ROE, ROIC and Interest coverage (last year Coca Cola had enough earnings to pay the interest costs 10 times) Source: Morningstar.com

Remember that companies can increase the ROE by taking on more debt. A good company generates enough money to finance most of its operations and does not need extensive debt. Amazon for example gets its money first and pays the suppliers after a month.

Margins and the One-Dollar Rule

High margins reflect that the business is able to ask prices for their products and services that a way higher than the costs. High margins and a fast turnover of assets (a business that sells it inventory quickly) means a high return on assets. Higher margins also leave more room to cut prices if needed. Businesses with moats have a sustainable higher margin than the competition over time. Competition could easily lower the margin of companies with no moat by offering the same service or product at a discount.

The earnings of a company can simply be retained or payed out to the shareholders. If retained earnings are invested productively, this should be seen by an increasing market price over time. If a dollar is retained than the market value of the stock should at least also go up by a dollar.

Management – "Operated by Honest and Competent People"

The quality of the management can greatly influence the amount of cash a company generates. Making investments with low returns, using too much debt, or buying back stocks at high prices can destroy shareholder value. Hence, management must be considered when calculating the value of a stock.

Warren Buffett's writings are well summarized by subject in the book of Lawrence A. Cunningham - The Essays of Warren Buffett. The following quote reflects how Warren Buffett thinks about good management:

"They love their businesses, they think like owners, and they exude integrity and ability. Just run your business as if: (1) you own 100% of it; (2) it is the only asset in the world that you and your family have or will ever have; and (3) you can't sell or merge it for at least a century."

The CEO needs to make the correct capital allocation decisions and needs to be honest and transparent to his shareholders. This includes telling shareholders about what goes well and what not. It can be quite easy to lose a lot of money by making acquisitions of companies for a price that is too high. The management should think like owners and be transparent to shareholders. That means not hiding problems in footnotes that are hard to understand for instance.

The news is full of "restructuring" stories. In such a case, a company that was acquired earns too little compared to the price that was paid. Then accountants can decide to decrease the value of the assets of the company if the earnings are too low (price paid over the asset value of a company (book value: what the company owns minus the liabilities) is listed as "goodwill" on the asset side of the balance). This must be written off from the income that a company earned (also known as impairment charges). And a lower net income often means a lower share price. Hence, we need a CEO that is able to make the right capital allocation decisions. Also, not taken up too much debt is essential.

At Berkshire Hathaway, most managers are wealthy and have no financial need to work. They work because they love their job! This is an important characteristic of good managers. Most managers at Berkshire Hathaway own substantial amounts of Berkshire Hathaway stock. It is often a good sign if managers buy their own stock.

A Very Attractive Price - Margin of Safety

The last step is determining the right price for your investment. Of course, after you assured yourself that you found a stable business, with a moat and good management. Successful investing can be summarized with three words: "margin of safety". Determining through facts and logical reasoning what something is worth and pay less for it. Note that "a very attractive price" was changed in 2007 to a "sensitive price" which better reflects that it is better to pay more for a good company than to have a bargain price for an average business.

Some Basics About Determining the Value of a Stock

The value of a stock is calculated by estimating the cash that the company will produce. The next step is to discount this cash flow (DCF). That means incorporating the fact that money that you will receive is the future is worth less than money that you receive today. This is also called "the time value of money". Imagine a US Treasury Bond that pays 10% interest. If you invest $100 for a year, the $100 will be worth $110 (100 * 1.10% = 110). If you divide the $110 over 1.10% you will get $100 (100 / 1.10% = 100). The latter calculation is called discounting (figuring out what something is worth today, given that you can invest it for a certain percentage).

This requires a stable and understandable company because you need to estimate how much cash will be available in the future. Furthermore, you need to understand and estimate the approximate growth rate of the company. Growth costs money, so you need to figure out if the costs of growing are higher, lower or equal to the amount of cash that the investments for growth will produce. Some companies need to spend most or more than their cash flow on expenditures for growth. This means that there is no money left for investors.

Intrinsic Value of a Business is a Range

Growth and value investing are often separated by investors. Warren Buffett says that growth and investing are "joined at the hip". Incorporating growth in your estimation is always crucial to calculate the value. Also, the value of a business is not a definite number. Rather, it is a range (e.g. between 100 and 110 dollars). This is because you need to account for positive, negative and neutral growth and cash flow scenarios for example.

In Security Analysis (the 1934 book by Benjamin Graham and David Dodd) you can read an example about the intrinsic value of Wright Aeronautical Corporation. In 1922, the stock was selling for $8 and earned $2 per share. That means an earnings yield of 25% (2/8 = 25%). In other words, you could earn back your money in 4 years (Price / Earnings of 4; 8/2 = 4). On top of this, the company had $2 per share in cash and a dividend of $1. The aviation sector had great prospects at that time, so $8 per share was a price below the intrinsic value of the stock.

In 1928 the stock price was $280 and the earnings only $8 per share! 280/8 = 35 times earnings per share. Now it was safe to conclude that the 35 times earning multiple was too high and based on unknown future prospects. The intrinsic value was lower than the $280 share price.

You can tell that a man is too heavy, but you cannot tell precisely how heavy. This example is also true for the example above. So, the intrinsic value is not definite, and can change due to changes business qualities (e.g. management or growth). However, the intrinsic value should always be justified by the facts: earnings, cash flow, outlook and management for example. A simple way of thinking about what to pay for a business based upon its earnings can be found in our previous article.

This book is the second favorite of Warren Buffett, and I think it is a great read as well for the serious investor.

Concentrated Investing – Why Warren Buffett Does Not Overdiversify

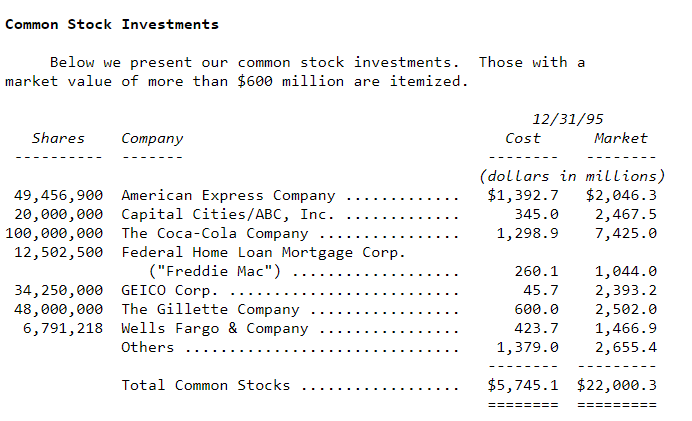

There are simply not that many understandable and attractive businesses around that can be bought for the right price. Hence, if you find one it pays of to invest a lot of your capital in something you like. You concentrate on the stocks you understand. This can be seen in the figure below. Almost $6 billion was invested in 7 businesses. At this moment, around 25 percent of the stock investments of Berkshire Hathaway is invested in Apple stock. Apple has a moat (strong brand and customer ecosystem), good management and this translates in a high cash flow, good margins and high return on equity.

Table of common stock investments of Berkshire Hathaway at the end of 1995.

The third best book according to Warren Buffett (The Intelligent Investor and Security Analysis of Benjamin Graham are number one and two) is Common Stocks, Uncommon Profits by Philip Fisher. Warren Buffett learned that if you buy a good business, the business tends to stay good over time. This means that the price of the stock will advance along with the success of the company over time.

"If the job (of selecting a stock) has been correctly done when a common stock is purchased, the time to sell it is—almost never." Philip Fisher Common Stocks, Uncommon Profits

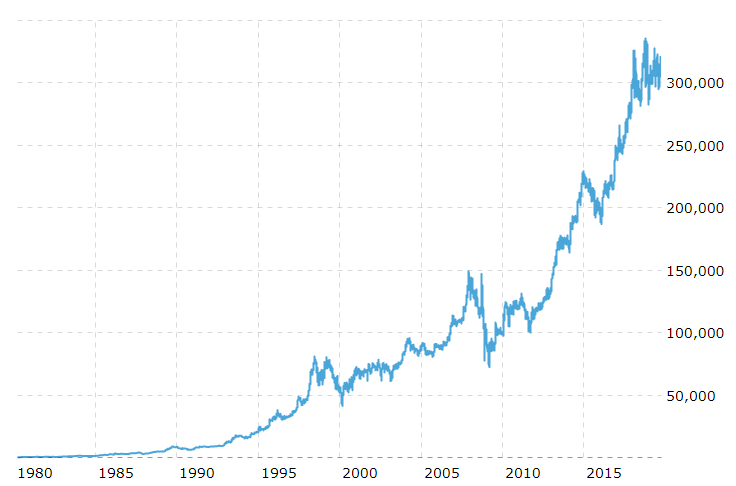

The key to the success is concentrating your investments in a few very good ideas and keep them for the long-run. Good businesses tend to stay good over time due to the lasting moat. One of the best examples is the stock of Warren Buffett, Berkshire Hathaway:

The power of compounding and long-term investing: Berkshire Hathaway advanced from around $300 to $300,000 between 1980 and 2019.

Source: www.macrotrends.net

Warren Buffett's Simple Investment Advice That Will Outperform Most Investors

Warren Buffett knows very well that most people do not have the discipline and knowledge to beat the S&P 500 over time. It is far better to grow with corporate America for most investors. It only requires the emotional stability and persistence to keep investing over time, without withdrawing money. Even better, you don't need to do any research if you chose to follow this strategy. Luckily, you can do this by buying an investing funds or ETF's that replicates the S&P 500.

Warren Buffett's Advice

In 2013 Warren Buffett mentioned that you can outperform most of the active managers by simple buying the S&P 500 via an index fund. The trick is to keep adding money over a long period of time and not withdrawing your money. The market is designed to transfer money from the impatience to the patient people is what Warren often says. Time is the friend of a good business (as it can increase sales and earnings over time). Economic developments will almost guarantee that economies like the US will do better in 10 or 20 years. It is almost impossible to determine what the economy is going to do next year, but in 20 years the US economy will be stronger and earning more.

In his letter to shareholders of 2013 he discusses what he gives some investing advice to his trustees:

"Put 10% of the cash in short-term government bonds and 90% in a very low-cost S&P 500 index fund. (I suggest Vanguard's.) I believe the trust's long-term results from this policy will be superior to those attained by most investors – whether pension funds, institutions or individuals – who employ high-fee managers."

In the book of John Bogle (the founder of Vanguard) you can read that it is very hard to outperform the market for most managers. Investing in an index fund that invests in the S&P 500 at low costs if very likely to outperform most of the managers. ETF's (exchange traded funds) are a great way to do this, although John Bogle does not like the fact that it is so easy to withdraw money from ETFs. So, he prefers an index fund which makes it harder to withdraw money in an instance. Warren Buffett and John Bogle were friends. Warren praised the way John made it easy for everybody to invest by developing index funds.

An ETF is a replication of for example an index. So, you can basically buy the shares of the 500 largest companies in the USA with one product. The key in successful investing is putting money at regular intervals (say monthly) in the S&P 500 and just wait for 10, 20 or more years. Your portfolio will follow the economic success of the USA in this case at very low costs (0.07% or less these days). Especially add money during recessions to benefit from the lower prices.

Summary

Warren Buffett invests by looking at four criteria. Although the principles are simple, the underlying analysis to find the correct business take more work. It includes knowing how the business operates, where its competitive advantage is, and it requires reading the annual reports. Years of accumulated knowledge is of a huge advantage here. And do not forget the emotional discipline and sticking to what you know and understand.

Remember, it is always better to buy a great company at a fair price than a mediocre business at a good price. Only very good businesses can grow at a rate that is higher than their costs of expending. This is plain economics: if a business makes a lot of money it will attract competitors. This will lower the prices you can ask to consumers. Unless, you sell for example cellphones with an Apple symbol on it. Apple has such a strong eco-system behind it that it is very difficult to successfully attack Apple's castle.

Over the long term, you are less likely to lose money. Never forget though, that the best company can still be a bad investment if you pay too much for it. That is why it is so important to be patient, follow a great company, and only buy at the right price!

Related Articles

- Warren Buffett's Investing Principles - Learn about the fundamental principles that guide Warren Buffett's investment decisions

- The Bird in Hand Theory - Understanding dividend investing and its importance in a value investing strategy

- How to Create an Investment Expectation - Classifying stocks into categories to develop realistic investment expectations